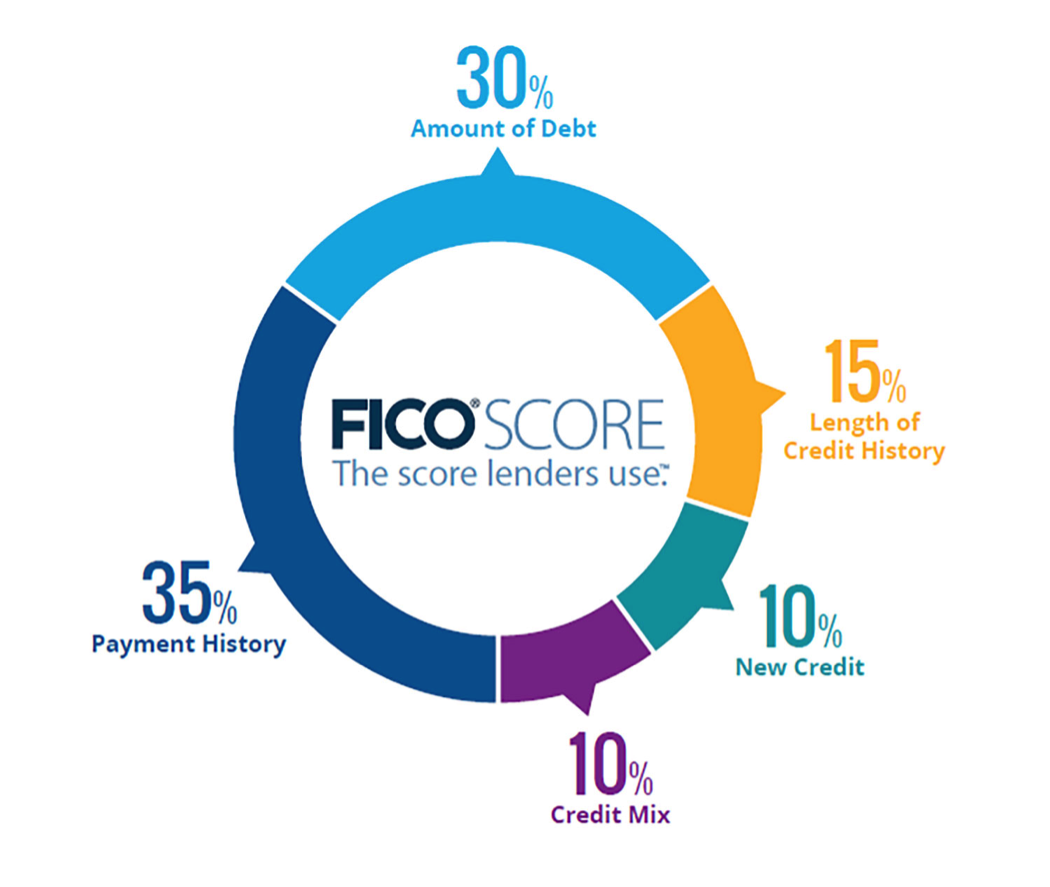

What is a FICO score and how does it work? This is a concern that puzzles even people seasoned in credit. The score is out of 850 and the higher the better… but where does that number come from? Luckily, FICO is more open about how their scores are calculated than other credit lenders, and show that your score boils down to five major facets with varying importance:

1. Payment History – 35%

The most important factor of a FICO score is the history you have with paying your accounts on time. As unfair as it may be given circumstances, negative items can remain for as long as 7 years! Credit agencies look at you chiefly like a model of predictive behavior: late payments in the past suggest you won’t pay on time. Thankfully, positive payment history remains even longer, as high as 10 years.

2. Amount of Debt Owed – 30%

The second most influential asset is how much remaining balance you have. Owing more is considered a risk to opening a new credit because it suggests you’ll behave similarly with the new account by racking up debt. Keep your credit card balances below 30% of your limit for the best results!

3. Length of Credit History – 15%

It’s also important to show how you can handle an account for long periods of time. The longer ago a current account was started, the better.

4. New Credit – 10%

Being able to open recent lines of new credit is proof to credit bureaus that creditors find you trustworthy.

5. Variety in Credit – 10%

It’s also best if your credit accounts are varied, having a mix of credit cards, retail accounts, mortgages, or auto loan shows you’re managing a lot of different accounts well.

THE BEST

THE BEST

signed up about two months ago, Raquel has been an amazing help, my scores for 3 bureaus already up 80 points. She has been the best. Very informative, whenever you need her she is available on the spot. Highly recommended. No matter how many questions you got, she will answer and explain everything. I really needed help with my credit and I'm so glad I went with this company. If you need help don't hesitate to reach out to them

I cannot recommend this company enough!! I was terrified with some of my debt and even called lawyers to see if they would help. Raquel gave me a free 30 minute consultation and got me from completely terrified to feeling at peace and with a plan in ONE phone call.

Being in debt is so scary and unfortunately there are a lot of shitty companies out there. Raquel and Fix Your Credit Consulting are a breath of fresh air and have the best care and attention for their customers. Schedule your call with them immediately and get a hold of your credit and finances!

The true sign of a business is one that could take your money, but instead tells you the truth that they can't help. I spoke with Sandra on behalf of a friend that had some credit issues and she determined that based on his report, she couldn't help him at this time. This company is wonderful and I would recommend to all friends and family having credit issues.

Thanks again Sandra for your honesty.

I've known Sandra for at least 10 years. She is a phenomenal person to work with and a super hard worker that cares about people. Do not hesitate to work with her and her amazing team. Jeff is wonderful as well!!

Thank you, team Fix Your Credit Consulting you are amazing*****